新用户扫码下载

新用户扫码下载

扫码下载APP

及时接收考试资讯及

备考信息

MA作为ACCA考试科目中较为基础的一门学科,其考试内容也比较简单,没有很多复杂的案例解析,因此学员可通过传统的记忆、背诵就可通过考试。以下为正保会计网校给大家汇总的MA科目中常见的公式,以供学员学习参考:

1. Equation of a straight line

y = a + bx

l y = total costs

l a = the fixed cost for the given period

l b = the variable cost per unit

l x = the number of units of activity

2. High-low method

Step 1 – select the highest and lowest activity levels, and their associated costs

Step 2 – find the variable cost per unit

Step 3 – find the fixed cost by substitution, using either the high or low activity level.

total cost at high activity level – total cost at low activity level

Variable cost per unit=

total units at high activity level – total units at low activity level

Fixed cost = (total cost at high activity level) – (total units at high activity level × variable cost per unit)

3. Free inventory balance

Materials in inventory

+ Materials on order from suppliers

- Materials requisitioned, not yet issued

= Free inventory balance

4. Economic Order Quantity (EOQ)

(Given in the exams)

Co = cost of placing one order

Ch = cost of holding one unit for one year

D = annual demand for stock item

Q = the order quantity

5. Economic Batch Quantity (EBQ)

(Given in the exams)

Q = the amount produced in each batch

D = demand per annum

Ch = cost of holding one unit for one year

Co = cost of setting up a batch ready to be produced

R = the production rate per time period (which must exceed the inventory usage)

6. Total Wages

Total wages = (hours worked × basic rate of pay per hour) + (overtime hours worked × overtime premium per hour)

7. Labor Turnover

No. of leavers who require replacement

Labor turnover = ---------------------------------------------- ----------------- X 100%

Average No. of employees

8. Labor Efficiency

Expected hours to produce actual output (standard hours)

Efficiency ratio = -------------------------------------------------------------------------------- × 100%

Actual hours to produce output

No. of hours spent working (active production)

Capacity ratio = --------------------------------------------------------------------------× 100%

Total hours available (budgeted)

Expected hours to produce actual output (standard hours)

Production volume ratio= -----------------------------------------------------------------------------× 100%

Total hours available (budgeted)

9. Absorption Rate

Overhead costs

Absorption rate = -------------------------------------

Volume of activity

Budgeted production overhead

Predetermined overhead absorption rate =-------------------------------------------------

Budgeted production activity

10. Marginal production cost

Marginal production cost = direct materials + direct labor + variable production overhead

Contribution = Sales – Variable cost

10. Marginal costing VS Absorption costing

If stock levels are rising, AC profit > MC profit

If stock levels are falling, AC profit < MC profit

If opening and closing stock levels are the same, AC profit = MC profit

Difference in profit = Change in inventory level × Fixed overheads absorption per unit

11. Conversion cost

Conversion cost = direct labor + production overheads

12. Correlation Coefficient

(Given in the exams) Where x and y represent pairs of data for two variables x and y n = the number of pairs of data used in the analysis |

Interpretation:

R = +1 perfect positive linear correlation

R between 0 and +1, positive correlation

R=0 no correlation

R between 0 and -1, negative correlation

R = -1 perfect negative linear correlation

13. Interest

l Simple interest

Where: V =Future value

X =Initial investment (present value)

r = Interest rate (expressed as a decimal)

n = Number of time periods

l Compound interest

Where: V =Future value

X =Initial investment (present value)

r = Interest rate (expressed as a decimal)

n = Number of time periods

l Effective interest rate

Where: r = Effective interest rate

i = Nominal interest rate

n = Number of time periods

14. IRR (using linear interpolation)

The steps in linear interpolation are:

(1) Calculate two NPVs for the project at two different costs of capital

(2) Using the following formula to find the IRR

Where: L = Lower rate of interest

H = Higher rate of interest

= NPV at lower rate of interest

= NPV at higher rate of interest

15. Payback Period

Payback period =

16. Annuity

PV = Annual cash flow X Annuity Factor

Annuity Factor:

17. Perpetuity

is known as the perpetuity factor

IRR of a perpetuity =

18. Variance

l Material price variance = Actual materials bought should cost-Did cost

l Material usage variance = (Actual output produced should use-Did use) × Standard price

l Labor rate variance = Actual hours worked should cost-Did cost

l Labor efficiency variance = (Actual output produced should take-Did take) ×Standard rate

l Variable overhead expenditure variance = Actual hours worked should cost-Did cost

l Variable overhead efficiency variance = (Actual output produced should take-Did take)× standard rate

l Fixed overhead absorption rate = budgeted fixed overhead / budgeted activity level

l Fixed overhead expenditure variance = Budget expenditure - Actual expenditure

l Fixed overhead volume variance = (Budget production volume in standard hours - Actual production volume in standard hours) × standard fixed overhead rate

l Fixed overhead volume Capacity variance = (actual hrs worked – budgeted hrs) × absorption rate

l Fixed overhead volume Efficiency variance = (standard hrs worked for actual production - actual hrs worked) × absorption rate

l Sales price variances = Actual sales units × ( Budget price - Actual price)

l Sales volume variances

(Budget sales units - Actual sales units) × standard profit per unit (Absorption costing)

Or × standard contribution per unit (Marginal costing)

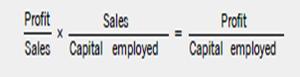

19. Profitability measures

l Gross profit margin = Gross profit /Turnover

l Net profit margin= Net profit /Turnover

l ROCE=Profit/capital employed

*Capital employed =total assets – current liabilities

=total equity plus long-term debt

Profit =profit before interest and tax (PBIT)

l Asset turnover= sales × capital employed.

l ROCE =net profit margin ×asset turnover

l Residual Income

RI=Controllable profit —Notional interest on capital

Notional interest on capital = the capital employed X a notional cost of capital or interest rate.

20. Liquidity measures

l Current ratio= current assets/ current liability

l Quick ratio = (current assets-inventory) / current liability

l Receivable collection period =trade receivables ÷ sales × 365 days

l Inventory turnover period=inventory ÷ cost of sales × 365 days

l Inventory turnover=Cost of sales ÷ inventory

l Account payable payment period = (payables/purchases) ×365 days

l Working capital period= (working capital/cost of sales) ×365 days

or = (working capital/ operating costs) ×365 days

l

21. Cost per unit of process outputs

Process cost | = | $( cost incurred - scrap value of normal loss - NRV of by-product + disposal cost of normal loss) |

Expected output | Input - normal loss |

22. Concept of equivalent units

The FIFO method

Cost incurred in current period

Cost per EU = _______________________________________________________________

Opening WIP *(1- 上期完工率) + 本期开工且完工产品 + Closing WIP*本期完工率

Weighted average method

Cost of opening WIP in last period + Cost incurred in current period

Cost per EU = _______________________________________________________________

Opening WIP + 本期开工且完工产品 + Closing WIP*本期完工率

——————————————

以上内容由正保会计网校原创整理、汇总编辑,转载请注明出处。正保会计网校拥有众多专业的ACCA教学老师为广大学员提供7x24H在线答疑服务,独有一键预约电话回访系统解您后顾之忧!更多资讯欢迎点我咨询!如需了解更多A考知识点欢迎点击>此处查看

推荐阅读:

下一篇:ACCA FA/FR考试常见公式

Copyright © 2000 - www.chinaacc.com All Rights Reserved. 北京东大正保科技有限公司 版权所有

京ICP证030467号 京ICP证030467号-1 出版物经营许可证 ![]() 京公网安备 11010802023314号

京公网安备 11010802023314号

![]()

新用户扫码下载

新用户扫码下载