新用户扫码下载

新用户扫码下载

扫码下载APP

及时接收最新考试资讯及

备考信息

2018年AICPA考试已接近尾声,2019年AICPA考试1、2月份的考位已经可以预约啦,你开始学习了吗?为帮助广大学员高效备考,正保会计网校美国CPA教学老师特别为学员总结了美国注册会计师考试《财务会计与报告》的常考知识点,以备迎接美国CPA考试,祝您在网校学习愉快!考试顺利!

● Types of inventory

● Goods included in inventory ☆

● Valuation of inventory ☆

· Costing flow assumption

· Lower of cost and market/net realizable value rule

● Periodic system and perpetual system

● Dollar value LIFO method

● Gross profit method

● Firm purchase commitment ☆

Types of inventory

● Retail inventory

● Manufacturing inventory

· Raw materials (RM)

· Work-in-progress (WIP)

· Finished goods (FG)

Goods to be included in inventory

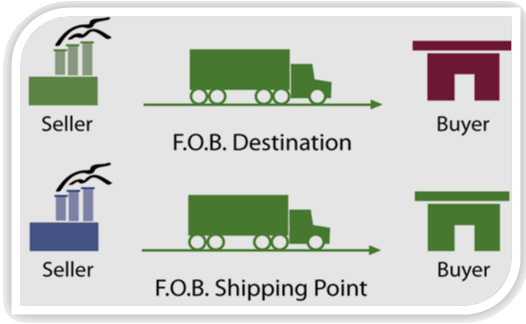

● Good in transit 在途存货

· Title passes explicitly agreed by parties

· If not explicitly agreed, title passes when seller’s performance regarding delivery is complete

Ⅰ.FOB shipping point

Ⅱ.FOB destination point

● Goods to be included in inventory

· Shipment of nonconforming goods

If the seller ships the wrong goods, the title reverts to the seller upon rejection by the buyer

Goods should not be included in the buyer’s inventory even if the buyer possesses the goods prior to their return to the seller

● Sales with a right of return (same as revenue rule)

· GR: seller’s inventory if the amount of goods likely to be returned cannot be estimated

· Exception: buyer’s inventory if five conditions met:

Ⅰ.Sales price substantially fixed

Ⅱ.Buyer assumes all risk of loss

Ⅲ.Buyer has paid some form of consideration

Ⅳ.Product sold substantially complete

Ⅴ.Amount of future returns can be reasonably estimated

● Consigned goods

· Seller (consignor) delivers goods to an agent (consignee) to hold and sell on its behalf

· Consignor’s inventory before selling to third party

● Public warehouses

· Who holds the warehouse receipt?

· Warehouse receipt evidences the title even though the owner does not have possession

· Goods stored in a public warehouse should be included in the inventory of the company holding the warehouse receipt

● Sales with a mandatory buyback

· Part of a financing arrangement

· Seller required to repurchase goods from the buyer

· Seller’s inventory even though the title has passed to the buyer

● Installment sales

· Seller sells goods on an installment basis but retains legal title as security for the loan

· Seller’s inventory if the percentage of uncollectible debts cannot be estimated

Valuation of inventory

● Inventory generally account for at cost

● Departure from the cost basis

· Precious metals and farm products: valued at NRV, which is net selling price less costs of disposal

· Lower of cost or market 成本与市价孰低

· Lower of cost or net realizable value 成本与可变现净值孰低

● Recognize loss in current period (write down)

· U.S. GAAP: Recognized in cost of goods sold or identified separately if the amount is material

· IFRS: not specified

● Reversal of inventory write-downs

· U.S.GAAP: prohibited

· IFRS: limited to the amount of the original write-down

● Lower of cost and net realizable value

· Apply to IFRS and U.S.GAAP (FIFO, average method)

· NRV = net selling price – cost to complete or dispose

· If BV > NRV, write down to NBV

· If BV < NRV, remain BV unchanged

● Lower of cost or market

· Apply to U.S.GAAP only (LIFO, retail method)

· Market value means current replacement cost, provided current replacement cost does not exceed net realizable value (market ceiling) or fall below net realizable value reduced by normal profit margin (market floor)

· Market value is the middle value of:

Replacement cost: cost to purchase

Market ceiling: NRV

Market floor: NRV – normal profit margin

Disclosure of inventory loss

· Substantial and unusual losses should be disclosed in the financial statements

· Small losses from a decline in value are included in the cost of goods sold

Periodic system 实地盘存制

· Beginning inventory + Purchase – Cost of goods sold = Ending inventory

· Quantity and value of inventory is determined only by physical count usually at least annually

· Cost of goods sold is squeezed

· Only one journal entry is recorded at time of sales

Perpetual system 永续盘存制

· Inventory record for each item of inventory updated for each purchase and each sales as they occur

· Actual cost of goods sold is determined and recorded with each sale

Primary inventory cost flow assumptions

Specific identification method

First in, first out method (FIFO)

Weighted average method

Moving average method

Last in, first out (LIFO)

● Additional explanation on LIFO

LIFO does not generally relate to actual flow of goods

If LIFO is used for tax purpose, it must be used in the GAAP financial statements

LIFO layers

Creation of LIFO layers

Increase or decrease of LIFO layers

● Dollar value LIFO

Regular LIFO: measured in units and priced at unit price

Dollar value LIFO: measured in dollars and adjusted for changing price

When converting LIFO inventory to dollar value LIFO inventory, a price index will be used to adjust the inventory value

Price index given

Price index computed as (ending inventory at current year cost) / (ending inventory at base year cost)

Gross profit method

● Used for interim financial statements as part of a periodic inventory system

● Inventory valued at retail, and the average gross profit percentage is used to determine the inventory cost

● Gross profit percentage is known and is used to calculate cost of sales

Firm purchase commitments

● Legally enforceable agreement to purchase a specified amount of goods at some time in the future

● If the contract price exceeds the market price, the loss should be recognized at the time of the decline in price

丨献给读者:越努力,越幸运!加油!!!

正保会计网校美国CPA以强大的师资队伍,精准的U.S.CPA题库,专业的考务服务为您的AICPA考试之旅保驾护航!

有意向报考的AICPA的考生赶快点击下方按钮进行免费预评估>> 了解AICPA报考条件吧!

![]()

Copyright © 2000 - www.chinaacc.com All Rights Reserved. 北京正保会计科技有限公司 版权所有

京B2-20200959 京ICP备20012371号-7 出版物经营许可证 ![]() 京公网安备 11010802044457号

京公网安备 11010802044457号

套餐D大额券

¥

去使用

新用户扫码下载

新用户扫码下载